Hospitality Insight

The shifting fundamentals of the UK hotel market

Market Trends and Future Outlook – H1 2025

We take a deep dive into the shifting fundamentals of the UK hotel market in eight key charts. Learn what they mean for owners, operators, and investors alike.

Recently we presented at the IHG Hotels & Resorts UK&I Owner and Investor Day at the spectacular Kimpton Fitzroy London — a day framed around a timely and powerful theme: Agile Partnerships and Lasting Impact. Joe Stather’s presentation focused on the shifting fundamentals of the UK hotel market — and what they mean for owners, operators, and investors alike.

In eight charts and slides we examine the demand outlook, the inflation paradox, and how leaders are coping with profitability pressure with a mix of strategies.

Review each visualisations, together with relevant discussion and analysis.

You can also download the charts in pdf format.

Author

Download Report

1. UK Demand Forecast – Positive Momentum, Moderate Pace

This chart looks at UK hotel demand, specifically in terms of rooms sold.

Of course, individual markets and properties will have varying levels of reliance on international demand which will impact the dynamic but for this baseline view, we’re focusing on aggregate UK hotel demand.

The chart shows a strong, long-term relationship between historic hotel demand and UK GDP — highlighted by the yellow and dark blue dots.

Over the 9 years to 2019, we saw a very high correlation of 0.97, with demand growing at a CAGR of 2.1%.

Remarkably, even during the pandemic period (2020–2024) — despite the volatility — that correlation increased to 0.98, with demand bouncing back at a CAGR of 23.7%.

Using this strong historical relationship, we’ve applied the latest UK GDP forecasts from both the OBR and the IMF to project hotel demand forward.

The OBR is slightly more optimistic, but both point to continued growth.

Our baseline scenario projects a CAGR of 0.6% from 2025 to 2029, translating to an increase from 200 million room nights sold in 2025 to around 205 million in 2029.

So while it’s not explosive growth, it is steady and positive — which brings us back to the message of this chart: positive momentum, moderate pace.

2. Elasticity and Resilience – The Inflationary Hedge Advantage

While we expect relatively modest growth in UK hotel demand, one key strength of the sector is its ability to convert favourable demand-supply dynamics into real rate growth.

Hotels have consistently demonstrated the elasticity to quickly translate increases in demand into price rises that outpace inflation. This characteristic is increasingly attractive to a broader range of investors looking for inflation-resistant assets.

Of course, this dynamic isn’t always positive — in some years, adverse conditions can lead to pressure on rates — but overall, the resilience of the sector remains a key advantage.

Turning to supply, it’s important to note that the numbers on the development pipeline are still adjusting post-COVID, so they may not be fully accurate yet.

However, it’s likely that supply growth will remain lower than demand growth in the short to medium term.

The total pipeline of new hotel rooms is declining,

The number of new project starts is also falling,

And this is expected to keep net supply additions limited, notwithstanding the outcome of properties under exclusive-use government contracts.

In summary this dynamic supports the outlook where moderate demand growth can continue to drive real rate increases, reinforcing the hotel sector’s position as an inflation hedge from a pricing point of view.

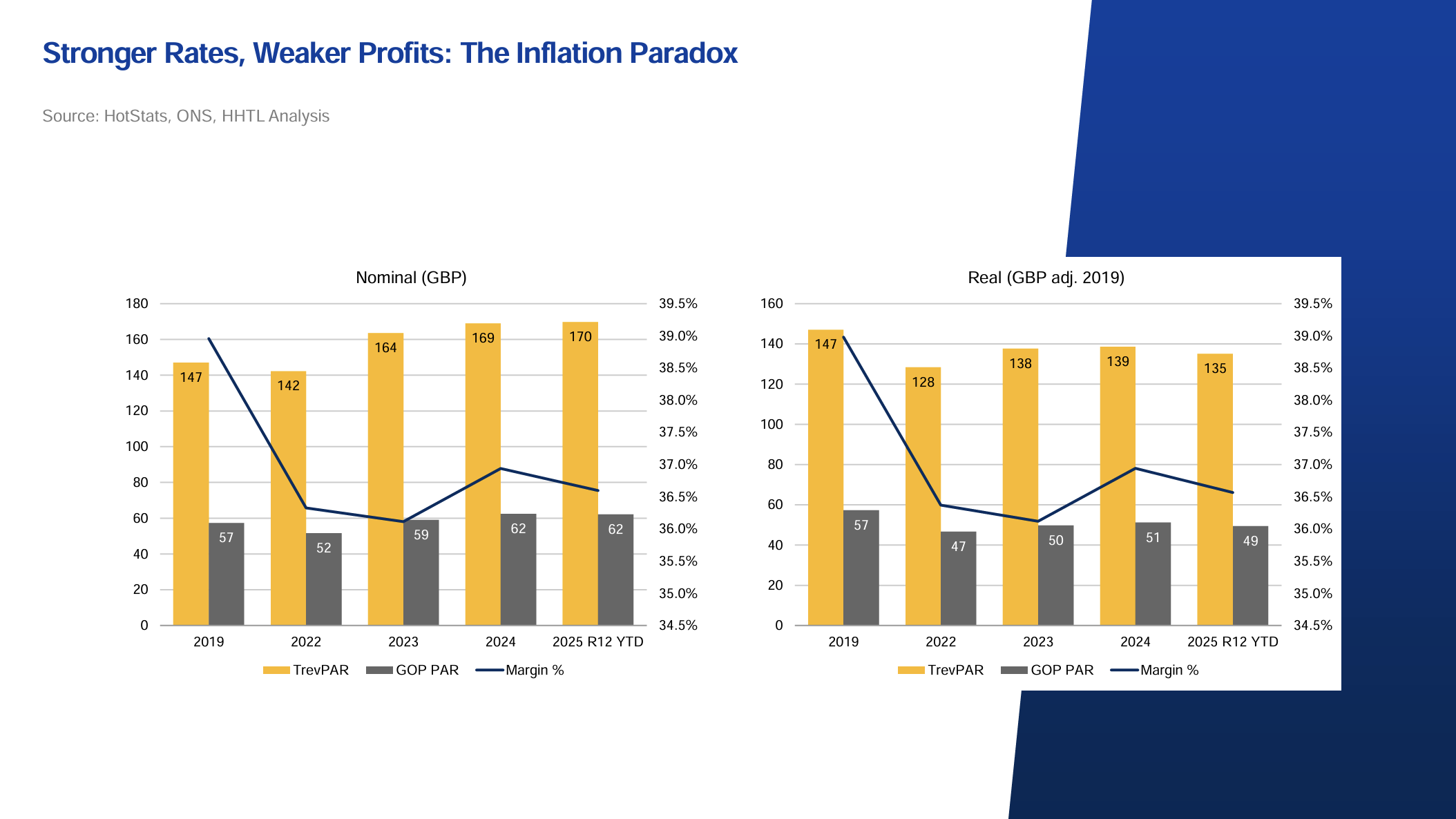

3. Stronger Rates, Weaker Profits – The Inflation Paradox

While room pricing remains a critical lever for performance, as we know, profitability is about more than just strong rates.

In our analysis. we looked at three key metrics:

- Total Revenue per Available Room (TRevPAR)

- Gross Operating Profit per Available Room (GOPPAR)

- Operating Margin %

The left-hand chart shows nominal performance over time. At first glance, the story appears positive: Total revenue has grown, and profits have recovered, despite a 3 percentage point drop in margin.

The takeaway here is that there’s been a lot of effort to deliver modest profit gains.

But the picture changes when we adjust for inflation.

On a real terms basis, total revenue is down by around £12 per available room between 2019 and 2025.

Even more strikingly, profit per room has fallen by 14%.

So yes, hotels remain profitable — but in real terms, they are less profitable than they were six years ago.

Despite strong room rates outpacing inflation, this hasn’t translated into real total revenue growth. Instead, cost inflation has eaten into margins, underscoring the ongoing challenge operators face in protecting profitability.

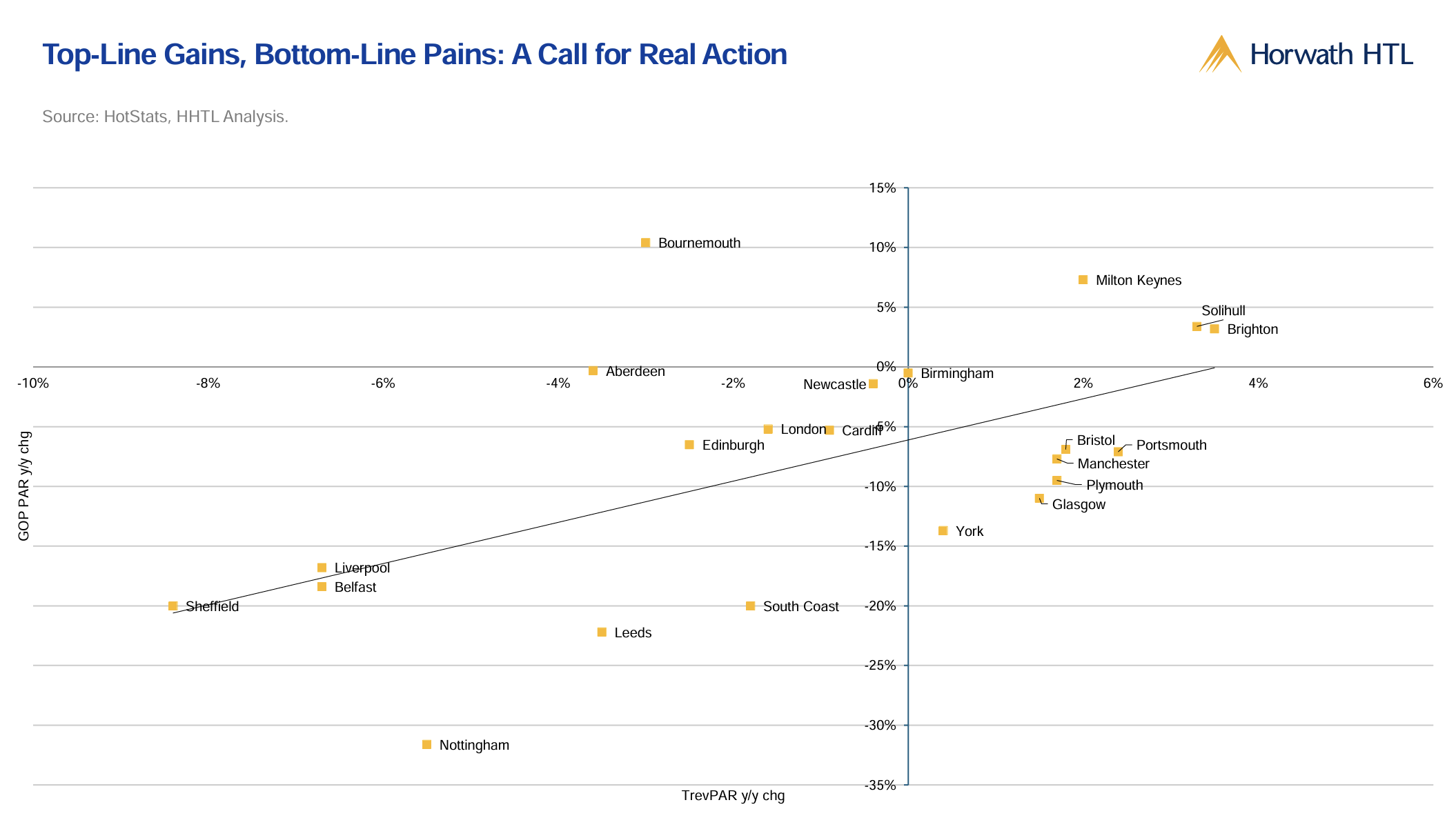

4. Top-Line Gains, Bottom-Line Pains – A Call for Real Action

This fourth chart really brings chart three into sharper focus.

We’ve plotted year-to-date % change in TRevPAR against % change in GOPPAR, market by market.

While we recognise that TRevPAR and GOPPAR don’t follow a strictly linear relationship, the trendline tells a clear story. Even with flat TRevPAR, we’re seeing a decline in GOPPAR of around 6%.

That’s a stark signal — a call for real action on operational efficiency and cost control, and a need to drive the top line, even if only as a defensive strategy.

Looking at the cluster of markets down in the bottom-right quadrant — Bristol, Portsmouth, Manchester and Glasgow these markets are seeing growth in total revenue, yet still suffering profit declines of more than 5% year-on-year.

There are some outliers, a few late-cycle bloomers, some resurgent MICE-driven markets and others affected by non-recurring events last year.

But overall, the pattern is clear: margin erosion is widespread, and it’s not going away on its own. The sector needs to respond with real operational discipline and strategic agility.

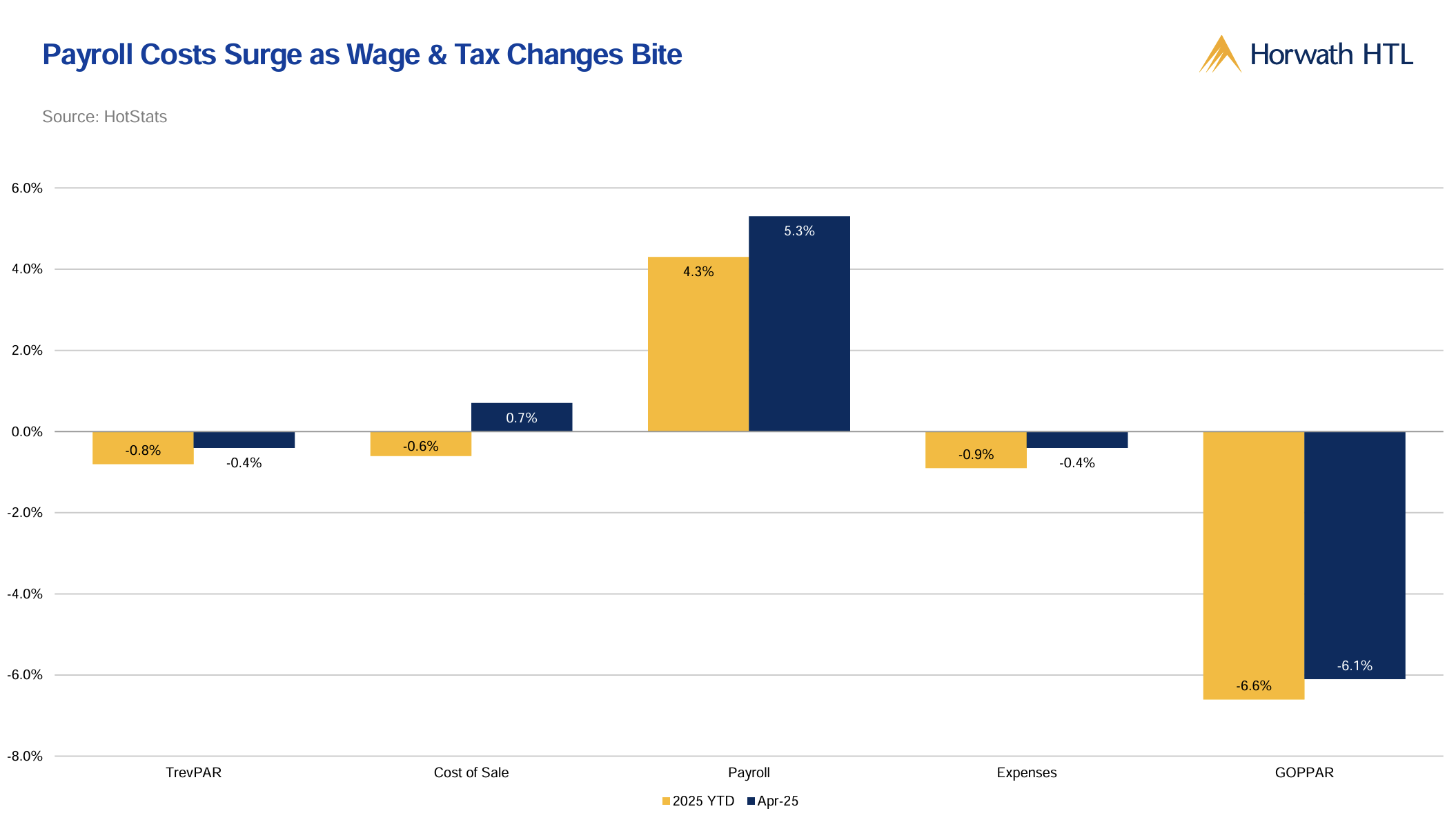

5. Payroll Costs Surge as Wage & Tax Changes Bite

Drilling down into what’s having the most significant impact on profitability, this fifth chart looks at year-to-date percentage change and the month of April year-on-year.

One thing is immediately clear – labour costs are the major pressure point.

In April alone, payroll costs were up 5.3% year-on-year.

Year-to-date, they’ve increased by 4.3%.

While we’ve seen energy price inflation ease, labour continues to exert intense and sustained pressure.

And it’s not just about pay rates — it’s a structural issue. Hospitality is a people-driven business; labour is a large and often inflexible component of operating costs.

The sector has been hit disproportionately by minimum wage increases, a tight labour market, and the ongoing impacts of immigration system changes, which are affecting staffing levels and flexibility.

All of this compounds to make payroll inflation one of the most significant headwinds to restoring or growing profit margins.

Golf

Wellness

Parking

Food & Beverage

Conference & Events

6. Guests Are Paying to Play, Park, and Unwind

Source: HotStats, Revenue POR R12 YTD

It’s not all doom and gloom. In fact there are bright spots, particularly when we look at ancillary revenue streams.

On a rolling 12-month basis, several non-room revenue categories are showing double-digit growth, signalling opportunities for diversification and incremental income.

Golf and wellness stand out as particularly strong performers.

Golf is growing from a low base, but the momentum is clear.

Both segments carry higher associated operating costs than rooms, but they tap into lifestyle trends and guest experience priorities.

Parking revenue is also growing strongly.

This reflects efforts by hoteliers to maximise wider land use, especially in suburban and regional locations.

There are also more modest gains in Conference & Events, up 2% year-on-year.

It’s growth, yes — but we all now recognise that C&E revenue has returned in a different guise compared to pre-pandemic patterns.

Food & Beverage is also up 2%, though in many cases, this isn’t enough to offset rising input and labour costs.

So while there are encouraging trends in ancillary revenue, particularly where assets and offerings are being more actively leveraged, the reality is that profitability gains will still require careful management of both revenue and cost across all streams.

7. Value for Experience

As discussed above, whether we’re talking about growing revenue, managing costs, or aligning with evolving consumer expectations, it’s increasingly clear that at all levels of the sector, differentiated experiences are a powerful lever for building brand strength, guest goodwill, and ultimately commercial return.

But what do we actually mean by experience?

We see three key components:

- Localisation

- Personalisation

- Activation.

Localisation is about creating a sense of place and authenticity. It anchors the guest experience in the local culture, community, and environment.

That could mean:

- Supporting local businesses and artists to foster social connection,

- Architecture and interior design that reflects the destination’s identity,

- Or storytelling that brings local history to life.

Personalisation makes the experience feel individual, thoughtful, and valued. It’s about using data and insight to anticipate needs and tailor moments — from small touches to seamless service journeys.

Done well, this builds emotional connection and guest loyalty.

And finally, activation — transforming passive spaces into dynamic, engaging environments.

Think pop-ups that encourage repeat visits, sensory stimulation, and opportunities to interact or participate.

It’s what brings energy and memorability to a space.

In short:

- Localisation grounds the experience,

- Personalisation makes it resonate,

- … and Activation energises it.

These three elements together offer a framework for creating value through experience — and that’s going to be key, regardless of chain scale, as we continue navigating this evolving market.

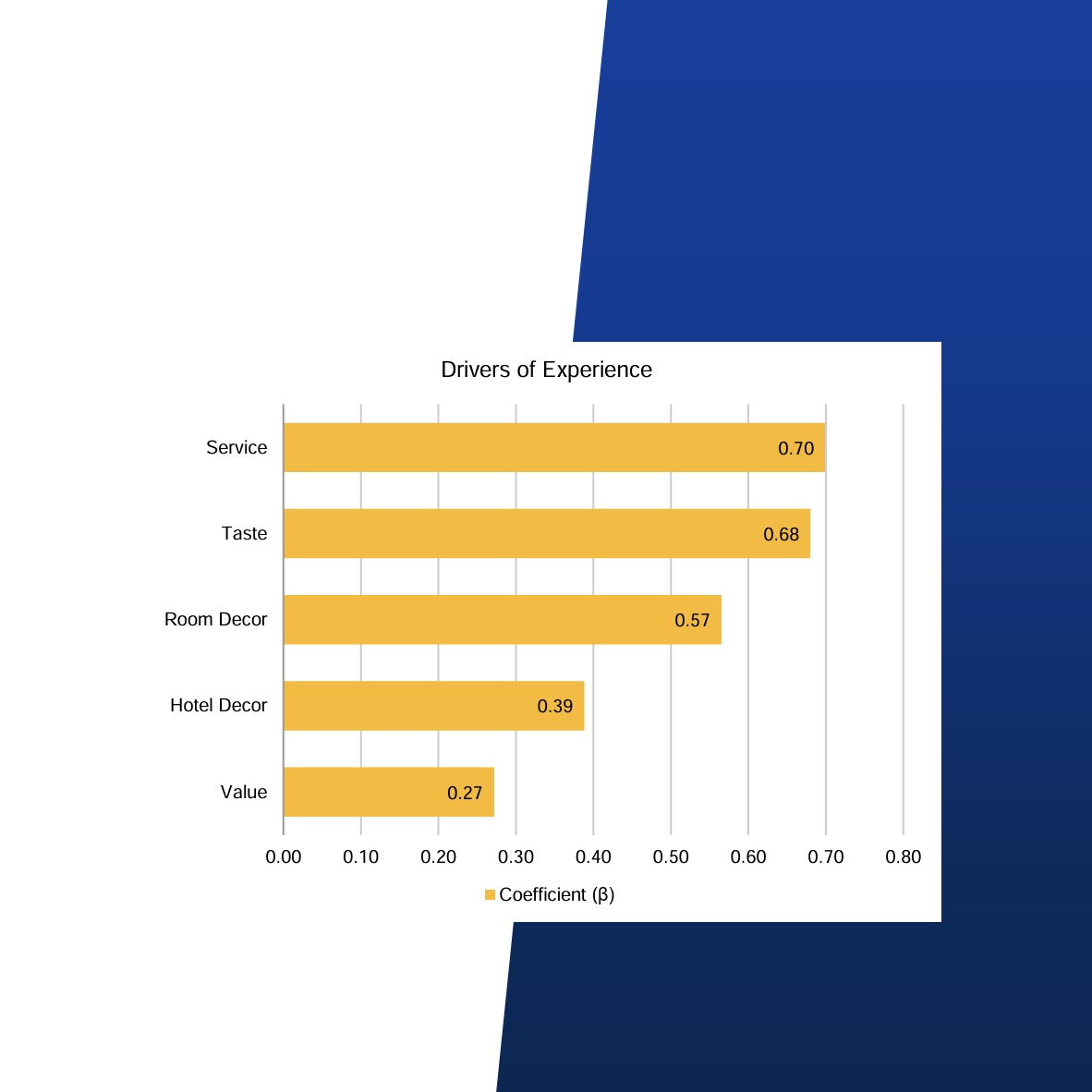

8. The Basics Still Matter

Source: Sorrel.ai, HHTL analysis

While strategies like localisation, personalisation, and activation are increasingly important for driving incremental revenue, it’s essential to remember that guest experience is still rooted in the basics.

According to analysis of data from Sorrel.ai, the factors most strongly correlated with guest satisfaction and value perception remain highly tangible:

First the service quality.

And secondly the physical condition of the hotel.

These core elements continue to have the greatest impact — regardless of how sophisticated or creative the experiential offer may be.

It’s also worth noting that “experience and value” — as captured in the dataset — actually has the lowest coefficient on the chart. In other words, a focus on experience alone doesn’t necessarily translate to a higher willingness to pay.

The key takeaway?

To truly leverage experiential enhancements into commercial returns, we must:

- Understand our customer segments.

- Tailor experiences that align with their specific values and expectations.

- And critically, communicate those enhancements clearly …

- … linking the perceived benefits to pricing, value propositions, and loyalty programmes.

Only by connecting the dots between experience, value, and communication can we turn creative strategies into measurable performance gains.

Take-aways

- Demand: Momentum is positive, but growth will be steady, not spectacular.

- Rates: Pricing power holds — supply lagging demand means inflation-beating gains.

- Profit: Costs, especially payroll, are eroding margins. Real profit recovery is tough.

- Ancillary: Golf, wellness, and parking show promise — but margins remain thin.

- Experience: Local, personal, and active experiences drive differentiation.

- Essentials: Service and condition still matter most — the basics can’t be ignored.

- Revenue: Turning experience into revenue requires sharp targeting and smart messaging.

About Horwath HTL UK

Horwath HTL is a specialist business line of Crowe, dedicated to the Hospitality, Tourism, and Leisure sectors.

We operate as a full-service consulting platform, combining deep sector expertise with the breadth of a global advisory network. Our team includes:

Sector specialists with hands-on experience in hospitality and tourism,

- A strong pool of experienced management consultants aligned with major investment themes,

- A leading corporate finance team,

- And experts in tax and structuring.

When it comes to hotels specifically, we act as independent advisors across key areas such as:

- Strategic planning,

- Development advisory,

- Due diligence,

- And asset management.

In short, we bring an integrated, end-to-end perspective to hospitality investment and operations.

Contact Joe Stather