Hospitality Insight

Canada Hotel & Chains Report 2024

April 2025

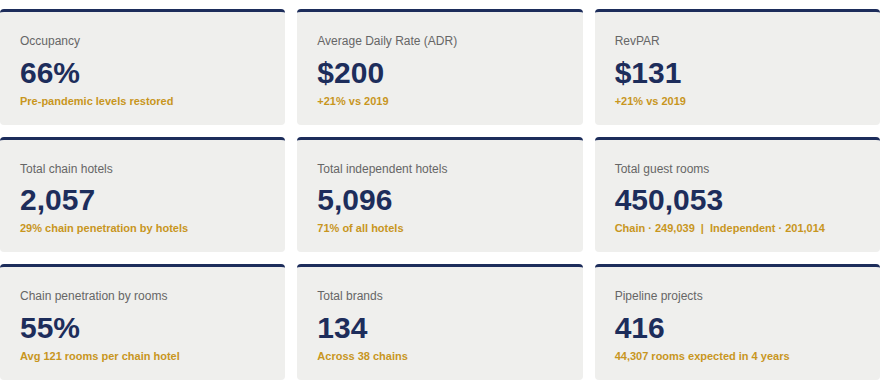

The Canadian hospitality industry has undergone a remarkable recovery since the lows of 2020. In 2023, hotels across the country reached pre-pandemic occupancy levels and posted record average daily rates, reflecting the resilience of both leisure and business travel demand.

This report, drawing on data from CoStar and Horwath HTL’s internal database, profiles a sample of over 7,100 Canadian hotels and nearly 450,000 guest rooms – examining performance trends, market structure, brand distribution, and the hotel development pipeline.

KPI’s

Market structure

- 71% of hotels are independent, but branded properties hold 55% of rooms

- Upper midscale is the dominant branded segment (33% of hotels, 28% of rooms)

- 60% of all hotels have fewer than 50 rooms — limiting franchise opportunity

- Ontario, BC, Alberta and Québec hold 83%+ of all guest rooms

Top brands & chains

- Marriott International leads by rooms (56,200); Wyndham leads by hotel count (482)

- Holiday Inn Express tops the brand list with 116 hotels and 12,302 rooms

- Comfort Inn has the most hotel locations of any single brand (141)

- Fairmont leads the luxury segment with 19 properties and 9,631 rooms

City performance

- Winnipeg recorded the largest occupancy gain since 2019 (+7.8 pts, to 76.1%)

- Banff achieved the highest ADR in Canada at $369 — up $87 from 2019

- Vancouver and Toronto remain among the highest-performing markets overall

- Western cities including Calgary, Kelowna and Saskatoon outpaced 2019 occupancy

Development pipeline

- 358 hotel projects expected to open within four years — up 10% year-on-year

- Toronto leads all destinations with 32 projects and 5,601 rooms planned

- Hampton by Hilton leads branded pipeline (22 projects, 2,592 rooms)

- Independent hotels represent 22% of pipeline rooms (9,700 rooms)

Authors

Download Report

Hospitality

Hotels & Chains Reports

Report